UK Property Supply Is Tightening. Here's What the On Invest Team Saw On The Ground

While headlines over the past twelve months focused heavily on whether UK property prices would fall, the reality on the ground is looking increasingly different.

According to the UK Office for National Statistics (ONS), both UK house prices and rents continued rising into 2026 – despite widespread expectations of a broader slowdown across the market.

The data highlights a wider trend that many developers and investors are now discussing more openly: while rental growth has moderated from post-pandemic peaks, underlying housing supply across many parts of the UK remains constrained. And, at the same time, regional growth markets continue outperforming.

The Market Rotated

The chart below shows where house price growth actually landed across England in early 2026.

The North West recorded the strongest annual house price growth of any English region. The West Midlands – home to Birmingham – also significantly outperformed the national average. London, by contrast, recorded a price decline for the sixth consecutive month.

This regional rotation is not a short-term anomaly. It reflects a deeper shift in where economic activity, corporate investment, and population growth are concentrating across the UK – and it has meaningful implications for where property values are likely to head next.

On the rental side, the trend is even more pronounced. Private rents across England have continued rising steadily, as the chart below illustrates – a trend that shows little sign of reversing given what is happening on the supply side of the market.

"Not Much Is Being Built" – The Supply Story Reshaping the Market

Last week, On Invest directors Siôn B. and John T. travelled across Birmingham and Manchester to visit completed projects, upcoming developments, and meet directly with developers operating on the ground.

The consistent message from every conversation?

Supply remains one of the UK market's most significant and underreported challenges.

"One of the biggest themes we kept hearing from developers across both cities was just how difficult it has become to bring new projects online. Planning delays and build costs are restricting supply at a time when demand in key locations remains extremely strong. That combination is going to push both prices and rents higher over the coming years."

— John T., Director and Co-Founder On Invest

This is the structural story that rarely surfaces in broader market commentary – but which matters most to investors thinking beyond the next twelve months. When supply is constrained and demand holds firm, rents rise. And, on the current trajectory, developers see no near-term resolution to the planning bottleneck that is keeping new stock off the market.

Birmingham: Demand Around the CBD Continues to Strengthen

In Birmingham, the On Invest team focused on prime city-centre locations within walking distance of the CBD and major corporate employers – HSBC, Goldman Sachs, and KPMG among them.

This remains one of the strongest-performing rental pockets in the city, and the reason is straightforward: the concentration of high-income professional tenants in this part of Birmingham is not driven by speculation. It is driven by the physical presence of some of the world's most significant financial institutions, which have established meaningful regional operations here and continue to expand them.

Birmingham also carries one of the youngest urban populations of any major UK city, providing a sustained base of rental demand that endures across economic cycles. Prime city-centre stock, in walkable proximity to these employers, commands genuine premiums — and vacancy rates in these locations reflect that.

On Invest clients have already secured positions in earlier stages of developments including Priors Gate and Paper Yard — exactly the kind of micro-locations where infrastructure, employment, and regeneration are converging simultaneously.

“The response we’ve seen to Priors Gate has been exceptionally strong, and for us, it further reinforces the underlying strength of Birmingham’s city-centre market. When you have limited new supply, rising rental demand, and prime locations positioned around major employment and regeneration corridors, the market is still extremely strong for the right product in the right location.”

— Siôn B., Director and Co-Founder of On Invest

Manchester: Infrastructure, Employment, and Visible Momentum

Manchester continues to demonstrate why it remains one of the UK's most closely watched growth cities – and one that rewards the attention of anyone who spends time in it.

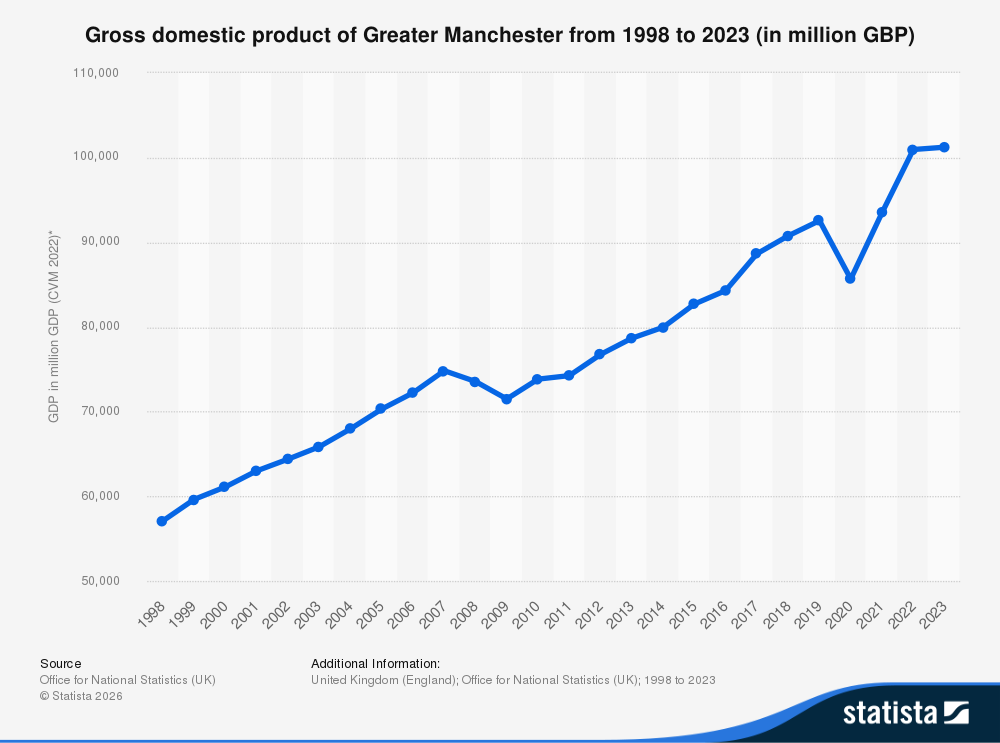

According to Bloomberg, greater Manchester's economy has been expanding at roughly twice the national UK rate, a trajectory that has attracted major global employers including IBM, Bosch, Booking.com, and Klarna to establish or grow regional operations in the city. The chart below shows how that economic output has compounded over time.

From the ongoing expansion of Manchester Airport to the commercial activity visible throughout the CBD, the scale of investment underway across the city is apparent to anyone walking its streets.

The team revisited Trafford Gardens, where more than 40 clients have now completed and successfully rented out their properties – a strong example of what the right location, at the right stage, can deliver. The neighbourhoods that were overlooked a decade ago – Ancoats, New Islington, Salford Quays – are now active, mixed-use districts attracting both residents and businesses at pace.

The team also walked the area surrounding Osborne Yard – where Siôn & John has previously placed a significant number of buyers, with just a couple of units still available – as well as Piccadilly Wharf, a newer launch in a prime area of Manchester City Centre, representing the next wave of opportunity in the city.

Where Does This Leave Investors?

While sentiment around the UK market has shifted over the past two years, the clearest takeaway from the trip was this: the supply constraints are real, they are deepening, and they are unlikely to resolve quickly.

Planning bottlenecks, construction costs, and slower development timelines are all contributing to a market delivering significantly less new stock than demand requires. At the same time, Birmingham and Manchester continue attracting businesses, infrastructure spending, graduates, and professional migration at a rate that the housing pipeline is not keeping pace with.

The conversation for investors, increasingly, is not about timing the market. It is about understanding where long-term structural demand is strongest – and positioning accordingly, before the window narrows further.

Location quality, walkability, employment connectivity, and genuine regeneration remain the determining factors. In the right parts of Birmingham and Manchester, those fundamentals are becoming harder to argue with.

If you're looking at the UK market and want to understand where the real opportunities are right now, get in touch. Our team is on the ground and ready to talk.